We look forward to serving you. Welcome to JPMorgan Chase.

Residential Leasing Market: We have yet to see any further evidence of weakness in the leasing market; this may be due to the fact that we have a limited sample size (our current homes available for rent), or it may be because, despite a weakening economy, margin home buyers who are priced out of purchasing a home are now well-qualified renters, buoying demand for rentals.

Mortgage Rates: Bankrate's national survey of large lenders has reported that the average interest rate on 30-year mortgages has decreased from 6.61 percent last week to 6.48 percent this week, in the midst of fluctuating mortgage rates due to a recent banking crisis.

As inflation takes center stage, the Labor Department has revealed that inflation decreased to 5 percent in March, its lowest level since 2021. The Federal Reserve has been taking assertive measures to control inflation, raising rates consistently for nine consecutive meetings since early 2022. These moves have put pressure on rates while increasing the possibility of a recession.

Lawrence Yun, the chief economist at the National Association of Realtors, believes that "calmer inflation means lower mortgage rates, eventually." He notes that March's 5 percent consumer price inflation represents a steady improvement from the high of 9 percent last summer, 8 percent in the fall, 7 percent during Christmas, and 6 percent in the early months of this year. While it may take about a year to reach the ideal inflation of 2 percent, Yun believes that the directional improvement is a clear signal for the Federal Reserve to change it's tightening monetary policy, particularly since many regional banks remain at risk of further interest rate disruptions.

Capital Market Commentary: Many high-net-worth home buyers over the last few years have been able to access cheap capital in exchange for putting large deposits in private banks or borrowing against their stock portfolios. These sweetheart loans are becoming rarer and rarer as interest rates rise. As we discussed in last month's "macro observations," when rates rise, the value of outstanding loans falls, which puts pressure on the bank. This is exactly what caused First Republics' issues. This poses the question - if these loans become more scarce, will that further cause demand to wane? The answer is yes.

Commercial Real Estate (CRE): It's starting to happen - 350 California Street, in San Francisco, is reportedly being sold for $60M. $60M sounds like a lot, until you realize it sold for $300M in 2019. If this transaction goes through, time will tell if the investor is a smart contrarian or if they are catching a falling knife.

What's The Good Word: Cancellation rates in homebuilding can also be an indicator of the broader economy. When the economy is strong and people have confidence in their ability to pay for a new home, the cancellation rates tend to be low. Conversely, high cancellation rates may indicate that people are struggling financially or are uncertain about the future, which can be a sign of economic weakness. Cancellation rates spiked in q4 2022 due to "mortgage rate shocks". Furthermore, a decline in cancellation rates may suggest that the housing market is stabilizing.

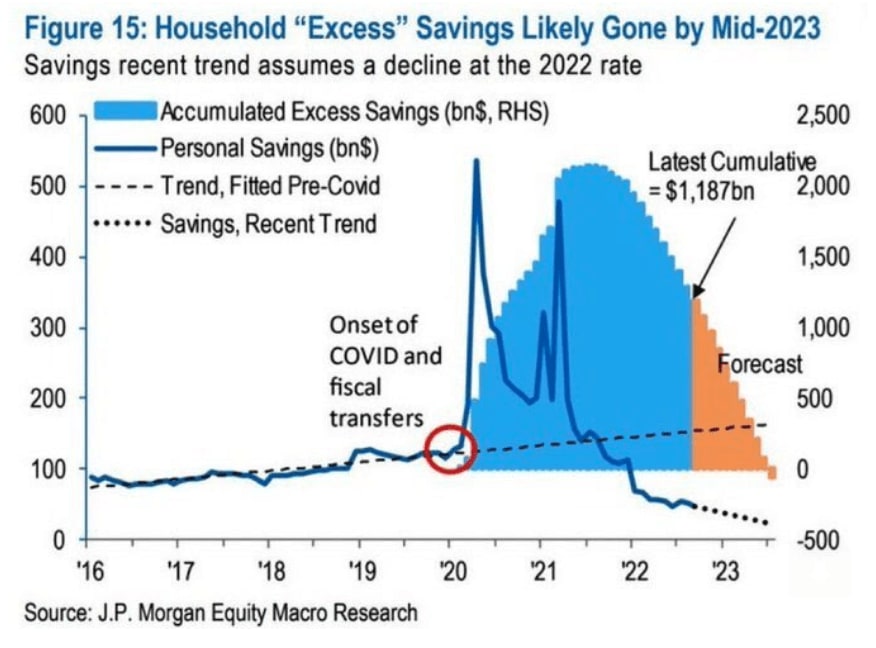

Macro Observations: it doesn't take a PhD in economics to conclude that the household savings trend (see chart from JP Morgan below) is a major headwind for the economy. The savings trend is likely driven by two main factors; the burning off of covid stimulus and the rampant inflation we all experience late last year.

Project Updates: We have several ongoing projects; here is a quick update on one of them:

Mission Drive, Costa Mesa: the ground has dried up, and footings have been dug and signed off. We are ready to pour foundations and then off to the races. Whereas our project on Placentia took 3 years from start to finish to build, we expect to complete this project within 2 years or less. The project on Placentia was 2nd of its kind in Costa Mesa; there was a big learning curve for all parties involved. If we do more of these, I think we can get the process down to 18 months.

On a side note, one of my new favorite things is to bring the girls along during weekend site walks. So far, Elizabeth seems to be interested in how buildings are made, and Kate (our younger daughter) daughter likes dirt and running across makeshift bridges.

If you, or your kids, are interested in joining us on future site walks, I'm going to be taking the girls to each major phase of construction and letting them see firsthand how homes are built. If you are interested in joining us, please let me know so we can coordinate.

Something Smart From Someone Smart: Dr. James Austin is a neurologist and author who has studied the neuroscience of meditation and its effects on the brain. In his book Chase, Chance, and Creativity, Dr. Austin describes four types of luck.

Blind luck: Hope that luck finds you.

Luck by persistence or luck by motion: Hustle until you stumble into it.

Luck by preparation: Prepare your mind and be sensitive to opportunities others overlook.

Luck by attraction: Become the best at what you do. Refine what you do until this is true. Opportunity will seek you out. Luck becomes your destiny.

*** The synopsis above is adapted from Naval Ravikant, a prominent entrepreneur and venture capitalist.

Dr. Austin's concept of the four types of luck provides a useful framework for understanding the role of luck in our lives and creative endeavors. It can help us increase our chances of success by being better prepared, open to new experiences, and resilient.

Book Rec: This is the true story of Bill Browder, a British political activist and financier of American origin, co-founded and currently serves as CEO of Hermitage Capital Management, which was once the top foreign portfolio investor in Russia. The story is a mix of James Bond meets Wolf of Wall Street. Browder took on the the Russian oligarchs, Putin and helped enact the Magnitsky Act (a controversial law created to help create accountability for Russian corruption). Overall, Red Notice is a very fun read and also provides some interesting perspectives on current geopolitical events.

Thanks again for reading. I hope this blog improves with time, and I would appreciate your feedback.

If there is anything you need: vendors, lenders, or other, please let me know. We have an extensive network of the best and brightest in the industry.

I geek off this stuff; if you want to grab coffee or chat about anything related to real estate, the market, or investing, please do not hesitate to reach out.